|

|

|

|

Slater Chronicles

January 2023

Wishing you and yours a safe, healthy and happy 2023.

With the recent announcement about the new First Home Savings Account (FHSA) as well as the increase to the yearly Tax Free Savings Account (TFSA) contribution limit, we thought a quick review of the key features and benefits of these accounts, as well as the Registered Retirement Savings Plan (RRSP), would be a great topic to kick off the New Year.

TFSAs, RRSP and the new FHSA account - which accounts make sense for you?

At first glance, the FHSA account appears to be an excellent option for anyone looking to buy a home. This account provides tax deductibility for your contributions, tax-free growth of the investments in the FHSA and the flexibility to withdraw the fund's tax-free to buy a home or transfer to an RRSP or RRIF if you decide not to buy a home.

While the final features and availability of the FHSA accounts are anticipated to be available on or about April 1st, 2023, here are the details available thus far.

FHSA:

- Any Canadian who is over the age of 18 and is a resident of Canada can have a FHSA as long as they haven't owned a home in the current year or the previous four calendar years.

- The FHSA will have an $8,000 annual maximum contribution limit, and unused contribution room can only be accrued and carried forward if an FHSA account has been established.

- The FHSA would allow first-time home buyers to save up to $40,000. Similar to an RRSP, contributions would be tax-deductible; like a TFSA, account withdrawals to buy a first home - including investment income - would be non-taxable.

- You can transfer funds specifically from an RRSP to an FHSA, subject to the $8,000 annual amount and $40,000-lifetime limits.

- If you don't buy a home within 15 years, the account must be closed. Any remaining funds in the FHSA can be rolled over tax-free into an RRSP or RRIF or withdrawn subject to taxes.

- The link to the government website containing the latest facts can be found here.

For younger Canadian who may be in a lower tax bracket at the start of their careers and have shorter-term goals like saving for a home, the TFSA or the new FHSA account may make most sense.

For longer-term goals, RRSP and TFSA offer key benefits for saving and investing, but there are other factors to consider, such as your age, income, and savings goals, when considering the best account to use.

For example, if you anticipate a higher retirement tax rate, a TFSA contribution may be more suitable than an RRSP. In contrast, if your tax rate in retirement is expected to be lower, then an RRSP may be a better first contribution option. If tax rates are expected to be similar in retirement, then the TFSA and RRSP offer similar benefits.

Key features of TFSA and RRSPs

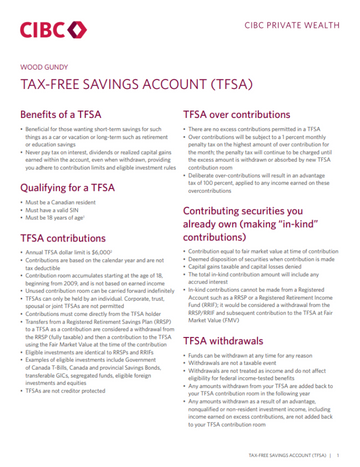

Tax-Free Savings Account (TFSA)

|

What Are You Saving For?

|

TFSA:

- The annual contribution limit for 2023 has increased to $6,500

- As of January 1, 2023, the maximum TFSA contribution is $88,000 if you have been a resident in Canada and were at least 18 years of age since 2009 but have never contributed in previous years.

- Contributions to your TFSA are not tax-deductible, and investment income earned in the TFSA and withdrawals from a TFSA are not taxable.

- Unused contributions can be carried forward indefinitely.

- Any amounts withdrawn from your TFSA are added back to your contribution room in the following year (except amounts withdrawn to correct an over-contribution).

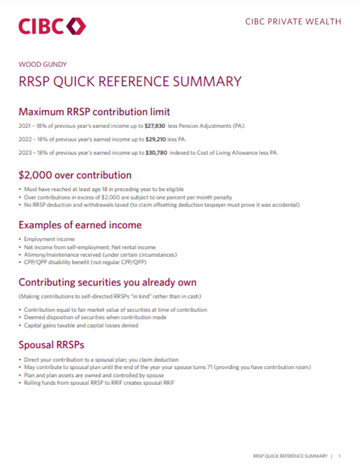

RRSP Quick Reference Summary

|

|

RRSP:

- You can make RRSP contributions up to 18% of your 2022 earned income, to a maximum of $29,210 less any Pension Adjustment, plus any unused contribution room from prior years and Pension Adjustment Reversal.

- The deadline to make an RRSP contribution for the 2022 tax year is March 1, 2023.

- Contributions to your RRSP are tax-deductible, and investment income earned in the RRSP is not taxable.

- Amounts withdrawn generally cannot be re-contributed.

- Withdrawals from an RRSP are taxable (certain exceptions are made for the Home Buyers' Plan or Lifelong Learning Plan if repaid following rules).

- You can contribute to RRSP in one year but claim the tax deduction in a future year.

While FHSA's, TFSA's and RRSP's all offer key benefits to help you achieve your goals, it's important to understand each particular situation to help you make the most informed choice.

|

Reach out to us

As always, we're happy to speak with you or your family members, friends or colleagues trying to figure out which accounts make the most sense for their situation.

|

|

Save The Date : "Death and Taxes" with Jamie Golombek, February 15 2023

This virtual event runs from 4pm to 5pm Eastern

Register Here

|

|

|

Since 1995 we've made ourselves available to act as a sounding board for anyone who may need urgent financial advice - or just a second opinion. We've been able to help many families. As a result, our business now comes to us almost exclusively through referrals. So, if you're approached by a friend, neighbour or family member, or if you know someone who needs a sympathetic ear, please let them know we will always find the time to listen, and we'll do our best to help. By making ourselves available this way, we're striving to make people's financial lives less stressful and better, and we're doing well by doing good. |

|

|

|

|

DISCLAIMER

CIBC Private Wealth Management consists of services provided by CIBC and certain of its subsidiaries, including CIBC Wood Gundy, a division of CIBC World Markets Inc. "CIBC Proviate Wealth Management" is a registered trademark of CIBC, used under license. "Wood Gundy" is a registered trademark of CIBC World Markets Inc.

|

|